Home Ownership in America

Buying a home is part of the American Dream. Home ownership generates stable and prosperous communities, allows families to put down strong roots and is one of the primary ways Americans build wealth. When a family owns a home, over time they build equity, or value, in it. Their home becomes an asset they can borrow against, pass down to their children or sell for a profit.

Imagine you worked hard, saved your money and wanted to buy a house in a nice neighborhood. But when you went to the bank to get a loan (which is how most people pay for a home), you were told no—because of the color of your skin, the neighborhood you wanted to live in or because you were deemed too risky to loan to. That was the reality for many Americans for much of the 20th century, thanks to a practice called redlining. Particularly targeted were people living in inner-city neighborhoods and Black-populated areas.

When people are denied mortgages to buy homes, they are also blocked from building wealth. This is why redlining had such a powerful and lasting impact. Redlining was officially banned decades ago, but its effects can still be felt today.

Neighborhoods that were once redlined often still have lower home values, less investment and fewer resources. Because homeownership is a major way families build generational wealth, past discrimination has created gaps that have been difficult to close.

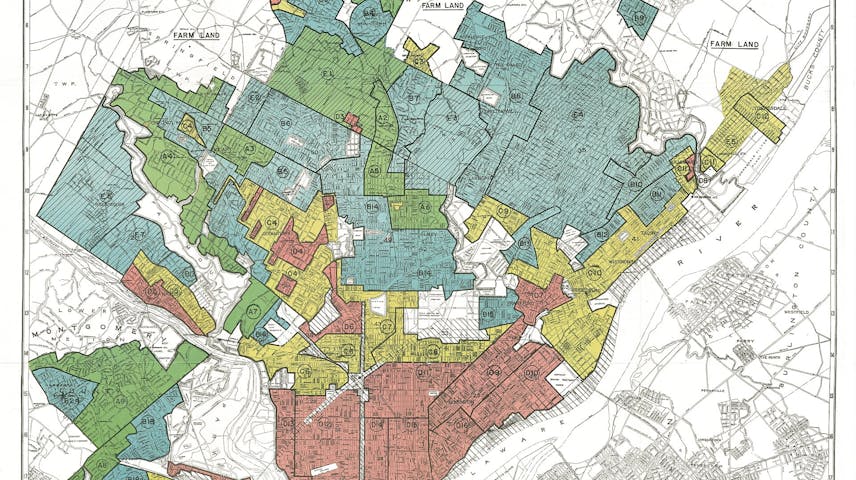

What Is Redlining?

Redlining is the illegal practice of denying people access to home loans—called mortgages—based on where they live. The name comes from actual maps that government officials drew in the 1930s on which neighborhoods were color-coded. The areas considered “hazardous” or risky for lenders were outlined and shaded in red.

How Did It Start? The 1930s and the Great Depression

To understand redlining, you have to go back to the 1930s. The United States was in the middle of the Great Depression, the worst economic crisis in American history. Millions of people lost their jobs, their savings and their homes. Banks were failing. The country was in trouble.

The federal government stepped in with a set of programs called the New Deal to help the economy recover. Two of these programs are at the heart of the redlining story:

The Home Owners’ Loan Corporation (HOLC) was a temporary program created in 1933 to help people who were in danger of losing their homes during the Great Depression. It refinanced struggling loans to give homeowners a second chance.

The Federal Housing Administration (FHA), created in 1934, worked differently. It didn’t deal with existing loans. Instead, it created an insurance system that backed new loans made by banks. This made it less risky for banks to offer mortgages with lower interest rates and longer repayment periods than ever before. Its goal was (and still is) to give mortgages to people with less money and credit and let them put less money down. The FHA makes homes more attainable for the less wealthy.

With a normal mortgage people traditionally have to put down, or pay, 20% of the house value, but with an FHA loan people can put down 3.5%. This makes it easier for a person to buy a home, but it also increases the risk of losing money for both the bank making the loan and the FHA. Because of this, the FHA made guides for the banks so that not too many of the loans would go unpaid.

To figure out where it was “safe” to back loans, HOLC and the FHA looked at neighborhoods across the country. They made maps using letters and colors on those maps to show which areas they believed were the safest—and riskiest—for banks doing the lending.

This may sound reasonable in theory, but in practice redlining made it nearly impossible to get a loan if you lived in the “red” or riskiest areas. The FHA’s actions shaped who got to buy homes and where in powerful ways. Researchers studying loan records from cities like Baltimore, Peoria and Greensboro found that the FHA consistently refused to insure mortgages for Black people. The FHA focused almost entirely on financing new home construction in the suburbs, which at that time was being built exclusively for white families.

Not Just Redlining

Restrictive Covenants: Discrimination Written into the Law

How explicit was the discrimination? Very. The FHA’s own 1938 manual warned against the “infiltration of inharmonious racial groups” into neighborhoods and recommended restrictive covenants, rules written directly into the deeds to homes (the official paperwork that describes a property) to exclude people, as a way to protect property values (“Redlining”). These covenants could say that a homeowner was forbidden from ever selling or renting their home to Black people, Jewish people, Asian Americans or other groups.

If a homeowner violated a restrictive covenant, they could lose money or even be forced out of their property. These rules helped keep entire neighborhoods all-white for decades, and they worked alongside redlining to limit where Black families could live. The federal government wasn’t just allowing discrimination—it was encouraging it.

Black Americans couldn’t get loans in inner-city neighborhoods, or Black-populated areas, because these areas were deemed “too risky” for loans. Nor could Black Americans secure loans in the “safe” suburbs, as they were faced with outright discrimination there. As aresult, redlining generated a self-fulfilling prophecy: areas deemed too risky for loans were starved for investment and so they declined economically, making them even riskier for loans. Many Black Americans found themselves “trapped” in deteriorating urban neighborhoods, unable to buy homes and unable to begin building wealth like white America was.

Blockbusting

Real estate agents added other harmful practices on top of redlining. One was called blockbusting: agents would warn white homeowners that Black families were about to move into the neighborhood, causing them to sell their homes cheaply in a panic. The agents would then sell those same homes to Black families at inflated prices, often through unfair contracts that offered no real ownership rights.

The Fair Housing Act and the Fight against Redlining

For decades, civil rights groups fought against these practices. Finally, in 1968, Congress passed the Fair Housing Act, which made it illegal to discriminate in housing based on race, color, national origin, religion, sex, disability or family status. Racially motivated redlining was now against the law.

The Fair Housing Act prohibited many specific practices, including:

Refusing to give someone a loan because of their race.

Charging higher interest rates because of a borrower’s race.

Placing a lower value on a home because of the race of people in the neighborhood.

The Equal Credit Opportunity Act provided further protections, making it illegal for lenders to use race or ethnicity when making credit—who they would loan to—decisions.

Federal agencies, including the Federal Reserve, were tasked with enforcing these new laws. It took time, and community groups continued to document cases where banks were still avoiding Black neighborhoods. The Community Reinvestment Act of 1977 pushed banks to serve all parts of the communities where they operated, including low- and moderate-income areas.

The Legacy of Redlining Today

Redlining was officially banned over 55 years ago, but its effects can still be felt today. Neighborhoods that were once redlined often still have lower home values, less investment and fewer resources than areas that were given green or blue ratings. Because homeownership is a major way families build generational wealth, the discrimination of the past created gaps that have been difficult to close.

Researchers continue to find that formerly redlined neighborhoods have lower rates of homeownership, lower median incomes, fewer trees, and in some cities, even worse health outcomes. The legacy is real, even if the maps themselves are long gone.

Today, federal law protects people from housing discrimination, and government agencies like the Consumer Financial Protection Bureau and the Department of Housing and Urban Development allow people to file complaints if they believe they’ve been treated unfairly in housing. But understanding how redlining worked—and how its damage is still felt today—helps us understand why housing equality remains an important issue.

Key Vocabulary

Equity—The value of a home that belongs to its owner, which grows as the loan is paid off.

Fair Housing Act—The 1968 law that made housing discrimination illegal in the United States.

FHA—Federal Housing Administration. This is the government agency that insures home mortgages for people with lower salaries or worse credit, so that they can still buy homes and put down lower down payments (often 3.5%). In the past, the FHA didn’t insure mortgages for Black homebuyers at the same rate as it did for white homebuyers.

HOLC—Home Owners’ Loan Corporation. This was a New Deal program that refinanced struggling home loans.

Mortgage—A loan used to buy a home, repaid over many years.

Redlining—The practice of denying loans or services to residents of certain neighborhoods.

Restrictive Covenant—A rule written into a property deed that limits who can buy or live in a home.

Self-fulfilling prophecy—An expectation about something that causes behaviors that make the expectation come true.